NVIDIA delivered a resounding answer to AI bubble concerns this morning, reporting third-quarter earnings that surpassed Wall Street expectations and signalling sustained momentum in AI infrastructure spending.

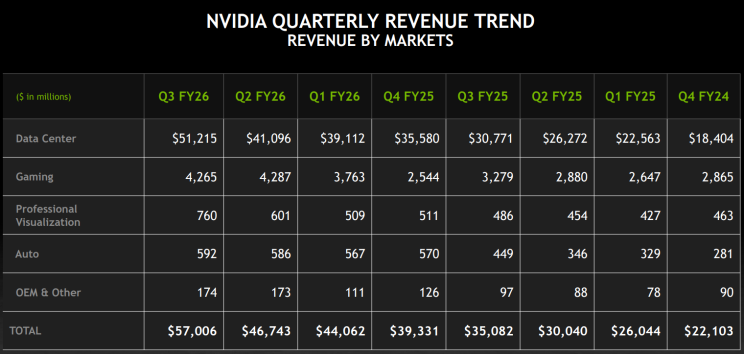

The chip giant posted adjusted earnings of $1.30 per share on revenue of $57.01 billion, beating analyst estimates of $1.26 EPS on $54.92 billion.

Revenue surged 62% year-over-year, with the critical data centre segment delivering $51.2 billion against expectations of $49 billion.

More importantly, NVIDIA projected fourth-quarter revenue of approximately $65 billion, significantly above the $61.66 billion consensus, indicating demand for AI accelerators shows no signs of cooling.

The company's next-generation Blackwell architecture is seeing unprecedented demand from cloud providers building out massive AI infrastructure. CEO Jensen Huang simply stated: "Blackwell sales are off the charts, and cloud GPUs are sold out."

NVIDIA shares had declined nearly 8% in November as prominent investors raised concerns about AI valuations. Peter Thiel's Thiel Macro completely exited its approximately $100 million position, while SoftBank divested $5.8 billion in holdings.

However, the continued capital expenditure by Big Tech customers — Microsoft alone spent nearly $35 billion in its most recent quarter, with roughly half allocated to chips — suggests the buildout phase is far from complete.

Beyond data centres, NVIDIA’s gaming revenue reached $4.3 billion (up 30% year-over-year), professional visualisation generated $760 million (up 56%), and automotive/robotics sales hit $592 million (up 32%).

The near-term trajectory remains strong, with the company continuing to capture the lion's share of AI chip demand in a market showing no signs of saturation.

Experts Split on Bitcoin's Trajectory

Bitcoin is at a vital inflection point, trading around $92,300 after briefly dipping below $90,000 for the first time in seven months.

The pressure stems from retail selling, leveraged trading liquidations, and institutional positioning, creating an environment where experts are split as to whether this is the end of the cycle or just a healthy pullback.

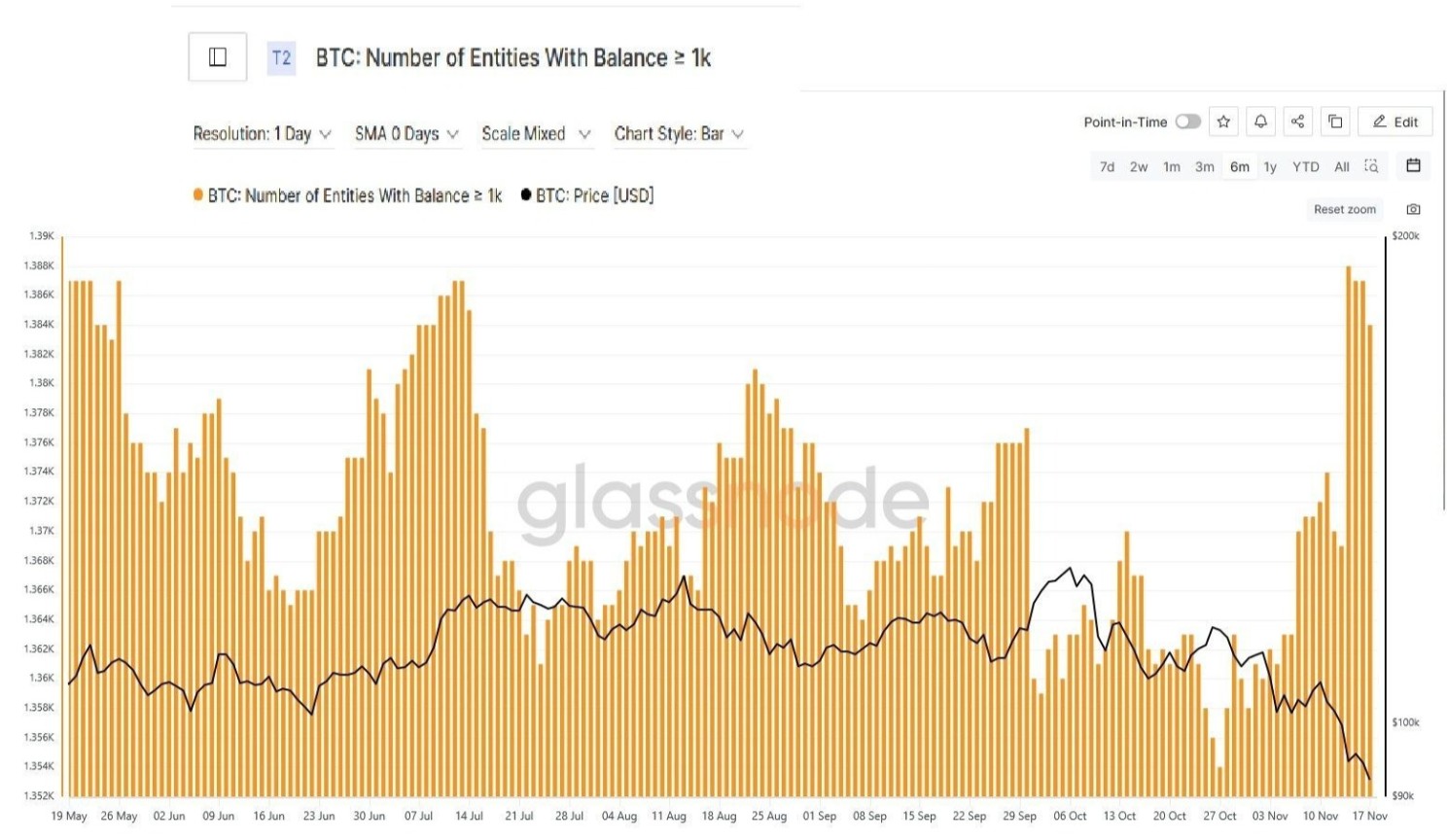

Glassnode data show approximately 65,200 BTC—valued at roughly $6.08 billion—was sold at a loss within 24 hours, indicating capitulation among short-term holders who bought near recent highs.

Yet, while retail investors panic-sell, wallets holding at least 1,000 BTC have increased to 1,384, a four-month high. Over 102,000 whale transactions exceeding $100,000 and 29,000 transactions over $1 million have been made this week, potentially making this the most active whale week of 2025.

This accumulation pattern during fear-driven selloffs has historically preceded medium-term recoveries (though past performance offers no guarantees).

For now, the market remains on a knife's edge, with high volatility seemingly the only certainty.

Fed Still Faces Divide as Data Starts Flowing

The Federal Reserve stands at a crossroads heading into its December 9-10 meeting, with internal divisions threatening to derail what was considered a near-certain third consecutive rate cut.

The released minutes of the October FOMC exposed strongly differing views within the Fed about the December policy decision, with many suggesting no more cuts are needed through the end of 2025.

.png)

Complicating things further is the data pause from the recent 44-day government shutdown. The Labor Department announced that October and November employment data won't be released until December 16 — six days after the FOMC meeting concludes — depriving the Fed of crucial labor market information.

Fed Chair Jerome Powell stated that a December rate cut is "far from a foregone conclusion," and there is "a growing chorus" among officials to "at least wait a cycle" before cutting again.

This represents the highest level of internal discord during Powell's tenure, with predictions of potentially four or five dissents at the December meeting — the most since 1992.

The December meeting will reveal whether the Fed can maintain the credibility needed to navigate a U.S. economy caught between stubborn inflation and (seemingly) weak labour market.

Every data release and Fed official comment between now and then will move markets as investors search for clues about the Fed’s next move.

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.